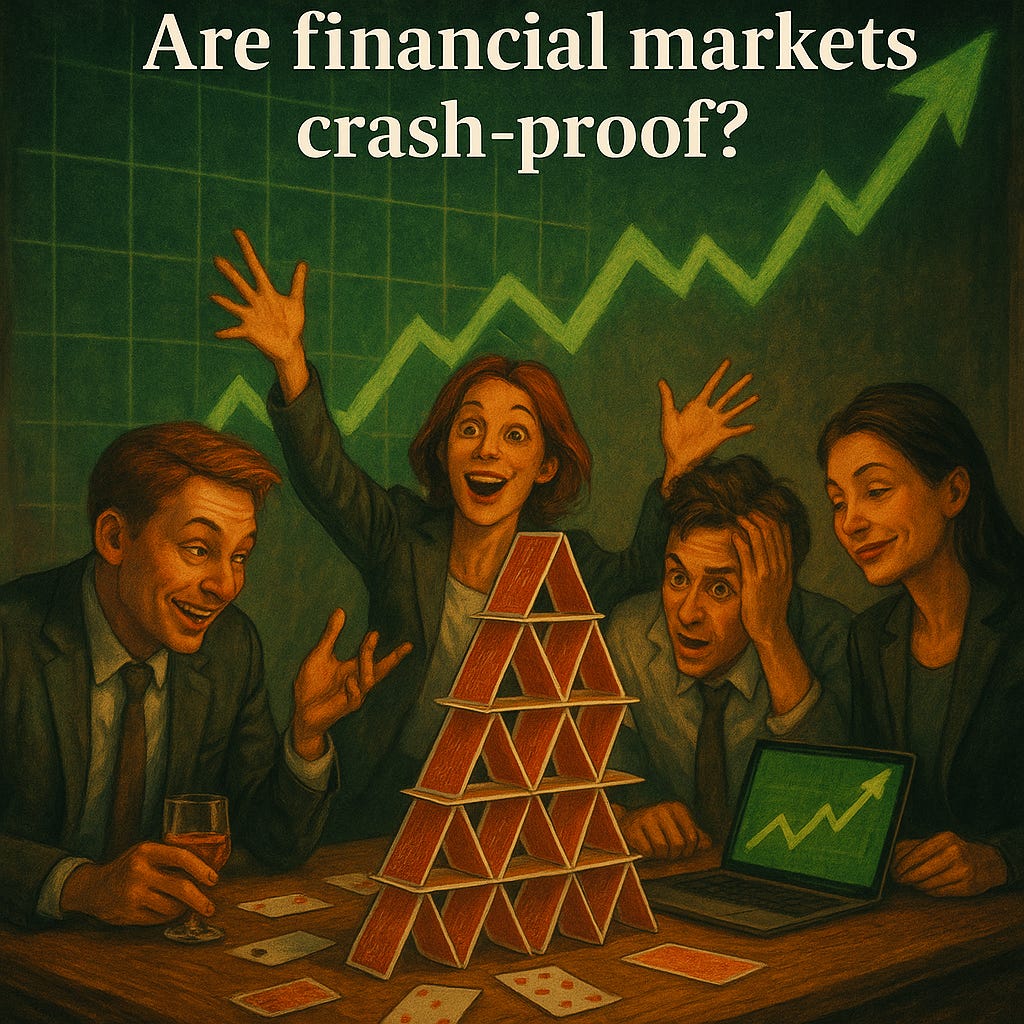

Recent market behavior has appeared remarkably resilient, even amid high-risk events such as the Iran–Israel war. This resilience has surprised many experienced investors and has prompted a closer examination of what truly supports current financial stability. The central question is not whether markets can absorb shocks for a time, but whether the underlying structure justifies the confidence often expressed in a supposedly crash‑proof system.

Since the 2008 financial crisisand accelerated by the COVID‑19 pandemicgovernments and central banks have expanded an extensive policy toolkit: fiscal stimulus, direct transfers, quantitative easing, liquidity backstops, and ultra‑low interest rates. These measures have cultivated a belief that policy intervention forms a robust safety net capable of neutralizing future shocks and smoothing economic cycles. In this view, growth seems predictable, asset prices defensible, and systemic risk manageable.

Evidence suggests, however, that such confidence may be overstated. Much of the post‑2008 policy architecture manages symptoms rather than resolving structural weaknesses. Monetary accommodation and fiscal interventions can stabilize demand and repair balance sheets temporarily, yet they do not remove the deeper causes of fragilitymost notably structural inequality, distorted incentives, and pervasive reliance on elevated asset valuations. Headline indicators can further mask vulnerabilities, creating an impression of health that is more cosmetic than curative.

Labor market data provides a clear example. While unemployment rates in many economies appear historically low, underemployment remains widespread. Skill‑mismatch, precarious gig work, and part‑time employment often substitute for stable, well‑compensated roles. Simultaneously, income polarization has intensified. CEO‑to‑worker pay ratios that hovered near 20:1 in the post‑war era surged to roughly 200:1 by 2008 and have continued to rise. Outsourcing low‑wage functions obscures true dispersion, and global labor arbitrage further complicates direct comparisons. The consistent conclusion is that income inequality has widened materially.

Asset prices amplify these pressures. Housing affordability illustrates how the cost of essential assets now shapes quality of life and demographic trends. In numerous urban centers, the transition from single‑income to dual‑income households has not restored affordability; even two salaries frequently fail to secure a modest home. Empirically, countries with rapidly rising property pricessuch as Canada and Australiaare observing declining fertility rates, indicating that asset inflation can carry long‑run social and demographic consequences.

Financial assets present parallel risks. Elevated valuations in equities, bonds, and investment property raise the cost of building a retirement portfolio while compressing expected future returns. This combination heightens sequence‑of‑returns risk, undermines retirement sustainability, and leaves households vulnerable to market drawdowns. Whether prices correct sharply or stay high, investors face a trade‑off between paying richly for uncertain future income and constraining current living standards to fund that exposure.

Together, these dynamics point to a deeper issue: the belief in crash‑proof markets reflects a potentially dangerous complacency. Fiscal stimulus and accommodative monetary policy can delay a reckoning, but they cannot indefinitely offset structural imbalances. When underemployment, income polarization, and asset‑price inflation persist, they operate as systemic warning lights. Ignoring these signals does not remove risk; it compounds it.

A constructive path forward aligns with ethical principles common to dharmic traditionsHinduism, Buddhism, Jainism, and Sikhismemphasizing balance, responsibility, and social harmony. Economic policy grounded in transparency, prudence, and compassion can reduce extreme inequality, strengthen household resilience, and ensure that markets serve societal well‑being. Such a framing neither rejects markets nor romanticizes intervention; rather, it recognizes that durable prosperity requires fairness, integrity, and stewardship alongside growth.

Practical vigilance therefore matters. Monitoring underemployment, wage dispersion, housing affordability, household leverage, fiscal deficits, and central bank balance sheets offers a more accurate assessment of systemic risk than headline unemployment or stock indices alone. At the household level, stress‑testing budgets, diversifying portfolios, and avoiding overreliance on asset appreciation can improve financial resilience without sacrificing long‑term goals.

In sum, financial markets are not crash‑proof; they are stabilizedat times impressivelyby policy tools that manage volatility but do not cure structural faults. Building a stronger foundation requires supply‑side productivity gains, inclusive labor markets, attainable housing, robust competition, and statistical transparency. Only through such reforms can resilience become intrinsic rather than borrowed from temporary interventions.

Inspired by this post on RightViews.